Twelve Years Later: How the K-12 Industry and Investment Landscape Has Shifted (Part 2)

April 5, 2019

Benjavisa Ruangvaree Art / Shutterstock

This is the second and final part of a series that explores how the market dynamics the K-12 education sector have changed. Read Part 1 here.

Twelve years ago, Amplify CEO Larry Berger and I wrote about the “pareto distribution” of companies in the K-12 sector. Most revenue was generated by a few winner-take-all companies, then there was a long tail of subscale operators.

The “oligopoly,” as we called it, was the natural outcome of a highly decentralized system and fragmented demand. To serve 15,000-plus districts and more than 100,000 school buildings, a company needed huge sales and service teams; to afford them, the company needed a bookbag full of products across content areas, grade ranges, and use cases. The structure of demand created the “Big Three”—McGraw-Hill, Houghton Mifflin Harcourt and Pearson.

Back then there were several of us caught in the middle of that distribution—growing companies such as Amplify, Curriculum Associates, iXL, Renaissance Learning and others. Our cohort has now grown to midsize-status, with over $100 million in revenue (and a couple over $200 million). And a new, growing class of companies may soon join us.

We broke through in different ways. Some went broad, hiring enormous sales forces to go building to building with supplemental products. Others went deep, with curriculum, intervention and assessment stacks. One way or another, each company built a channel big enough to pull its products through and assembled enough of a product mix to support that channel. Growth largely came at the expense of the “Big Three.”

Meanwhile, the number of small players—further right on the pareto distribution—has grown dramatically. Online distribution and freemium business models have enabled companies like Flocabulary, Newsela, Nearpod, and others to reach tens of millions without traditional “feet on the street.” But after a certain point, many of them realize that the next stage of growth requires real sales muscle.

All of these players, new and old, are operating in a stable yet fragmented market, finding product-market fit in school systems’ existing market segments: core, supplemental, and assessment. (I exclude technology from this analysis). If you bucket all instructional materials—core plus a broad view of “supplemental”—you have an estimated $6 billion instructional materials market. Assessment (including state tests) is another $1.2 billion or so.

Over years and decades, spending has shifted among these segments: the assessment market grew following the adoption of the Common Core; supplemental spending is catching up with core. In each segment, digital content is (slowly) eroding print. There are macro trends too, such as a pull-back in buying following the Great Recession. But the structure of the market remains essentially unchanged: narrow segments defined by content and grade, each with their own sets of buyers, rhythms and requirements.

The good news is, the segments represent real demand; the bad news is that they’re saturated. Tackling the $6 billion instructional materials market almost always requires displacing a product, program or service already in use. You’re competing for the dollars, but also for the school’s attention. When are they going to find the time? It’s easier when it feels familiar.

NEWSLETTERS

STAY AHEAD IN EDUCATION.

Sign up for EdSurge newsletters for timely news, insights and analysis.

Consider Archipelago Learning. Launched in 2000, it developed Study Island, a computer-based test-prep software tied to state standardized tests. It was a technology company, delivering test prep on a computer screen instead of in a paper workbook. Its use case (test prep), the spend model (per pupil per year), and the funding stream used (more than a little Title I) was comparable to publishers like Vantage Learning.

It’s a repeatable growth play: new entrants displacing established publishers. Vulnerabilities vary: aging copyrights, failure to address new standards, outdated technology and distribution channel issues. Several years ago, two of the “Big Three” integrated their supplemental and core sales forces. Their supplemental businesses shrank as a consequence, and opportunity emerged for a new cohort of intervention players.

If you don’t want to target existing segments, there are a few alternative models to consider.

The first includes the “eyeballs-first” players—companies like Remind, ClassDojo, and Edmodo, who all adopted a “West Coast” approach: collect active users now, with plans to monetize later. I’m more East Coast, and admit to struggling to understand the West Coast approach. Because targeted advertising is—appropriately—off-limits, and teachers don’t usually have pursestrings, a sustainable business requires a creative model. Edmodo didn’t find one; Remind has started to sell premium services to schools and clubs; and ClassDojo is marketing to parents. Time will tell how these strategies play out.

The second includes the “platform” players—Schoology, itslearning, Canvas, and other LMS-like platforms. They have set out to do something differently, only possible by means of technology—to be the search, storage and distribution platform for instructional content. But widespread usage—which I define as the majority of K-12 teachers using a district-adopted LMS every day—is elusive. Google Classroom has instead emerged as the de facto standard platform, fueled by the runaway adoption of Chromebooks.

The third includes “policy responsive” players—companies like Panorama, Ellevation or Wireless Generation in the early days. These companies help school systems meet a new policy requirement—social-emotional learning, English Language Learning, and reading assessment, respectively. Policy winds create meaningful opportunities to grow and serve, representing the closest thing we have to “new markets” in K-12. But long-term growth requires either tacking into new policy winds or finding one of the big existing markets.

So what is the state of the industry? On the one hand, it is an exciting time of transition. The big players are struggling, the market is more open to midsize providers, and even small competitors can get scale via social marketing and online distribution. On the other hand, the fundamentals of K-12 demand are mostly unchanged. Schools spend on content, activities and tests, then piece them together. School budgets are relatively flat year to year, and so growth tends to be zero-sum. And yet investment keeps pouring in.

K-12 Investment Landscape

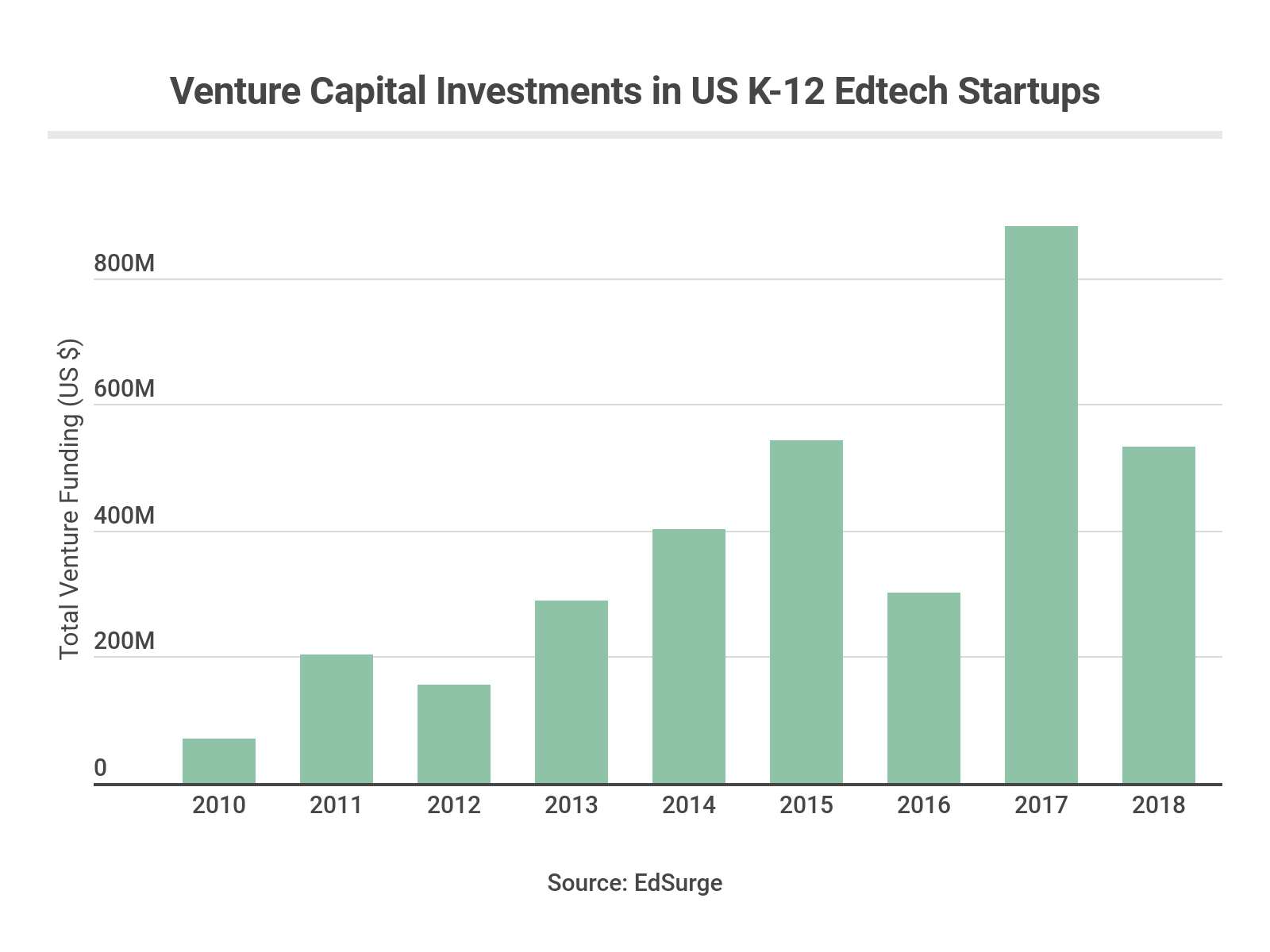

Twelve years ago Larry Berger and I said the leading barrier to entrepreneurship in K-12 was that “The Education Sector Does Not Invest in Innovation.” Venture funding was scarce. That’s no longer the case.

Now there’s a large and growing edtech investment industry. Owl Ventures recently raised its third fund—to the tune of $315 million. Reach Capital, New Markets Venture Partners, Rethink Education, and many more are in the mix. Supply of new companies has reached a fever pitch. Entrepreneurs are putting more productive tools in teachers’ hands, delivering more engaging instruction to students and supporting system redesign around new models.

At the same time, private equity money is also flooding into the sector. TPG’s Rise fund, Insight Venture Partners, and new players like CIP Capital Partners are doing a mix of late-stage investments, buyouts and rollups. These seem like savvy bets. Developing and maintaining a sales and marketing channel can be a lot for a single-product company in K-12. It’s more efficient—and more durable—to distribute a collection of adjacent products. Pearson isn’t buying startups any more, and private equity is seizing on an opportunity.

So smart capital is going to work finding the right mix of channels, services and products that meet the market’s needs. The midsize players should have an opportunity to bulk up, and I suspect we will wind up with a “Big Six” or “Big Eight.” The market is slowly recovering from decades of stifling oligopoly.

What about the ‘clutter’?

But we’re not “decluttering” our classrooms or in our schools. Entrepreneurial supply is still feeding fragmented demand. The stuff—software logins, workbooks, kits—continues to pile up. That hero teacher is still in charge of synthesizing it all.

Instead of inviting vendors in to work on program design and implementation, K-12 buyers keep them at arm’s length. In private-sector enterprise software, sales is an act of “joint value creation,” meaning it’s the sales rep’s job to understand the prospect’s business problem, design a solution, and demonstrate the likely return on investments. But the idiosyncratic K-12 buying process is rarely a means of joint value creation.

What would it take for the private and public sectors to work shoulder-to-shoulder?

One possibility would be for districts and providers both to edge towards integrated instructional models. Doing so would require a high level of collaboration on the demand side—with adequate planning time for district staff to work on integration and implementation planning in advance of procurement. The assessment team would need to get comfortable with curriculum-connected assessments that also provide meaningful data in aggregate. Intervention teams would need to balance alignment with the core materials—for example, in terms of letter sequences and content—while planning varying approaches and scaffolding to help all learners.

For the publishers—especially the mid-size growth players—edging in this direction would suggest that product lines evolve over time to integrate with one another. Most have done some work on the issue, but rarely at depth. It’s a catch-22: so long as buying is fragmented, it’s hard to justify the integrated product investment; so long as products are fragmented, it’s hard for a district to create an integrated instructional model.

To stretch the field, school systems could instead lead with a desired outcome and an initiative budget. Accept proposals that integrate across product and service segments. Make a portion of the fee contingent on outcomes, such as implementation integrity or student achievement results. Clear out the closets to make room for a focused effort.

The alternative is to continue to pile up the clutter. But I believe that we, collectively and collaboratively, can do better.

Dave Stevenson (@dbstev) is Entrepreneur-in-Residence at Whiteboard Advisors and a former executive at Amplify Education.

Popular on Edsurge

Opinion