US Edtech Closes Decade with Record $1.7 Billion Raised in 2019

By Wade Tyler Millward and Tony Wan

January 15, 2020

By andrea crisante / Shutterstock

Two trends have helped to define the U.S. economy leading into 2020—equity market milestone after milestone plus a historically low labor pool. In 2019, the Dow Jones Industrial Average passed 28,000 points, the S&P 500 Index topped 3,000 points and the Nasdaq broke 9,000 in what some have termed one of the longest bull markets in history.

At the same time, employers have sought third parties to help recruit top talent or develop it among existing employees. Economic factors outside employers’ control have spurred this need for outside help—it’s hard to hire when the unemployment rate is at a low of 3.6 percent, not seen since 1969 (a low perhaps spurred by a low workforce participation rate as people give up on applying for jobs).

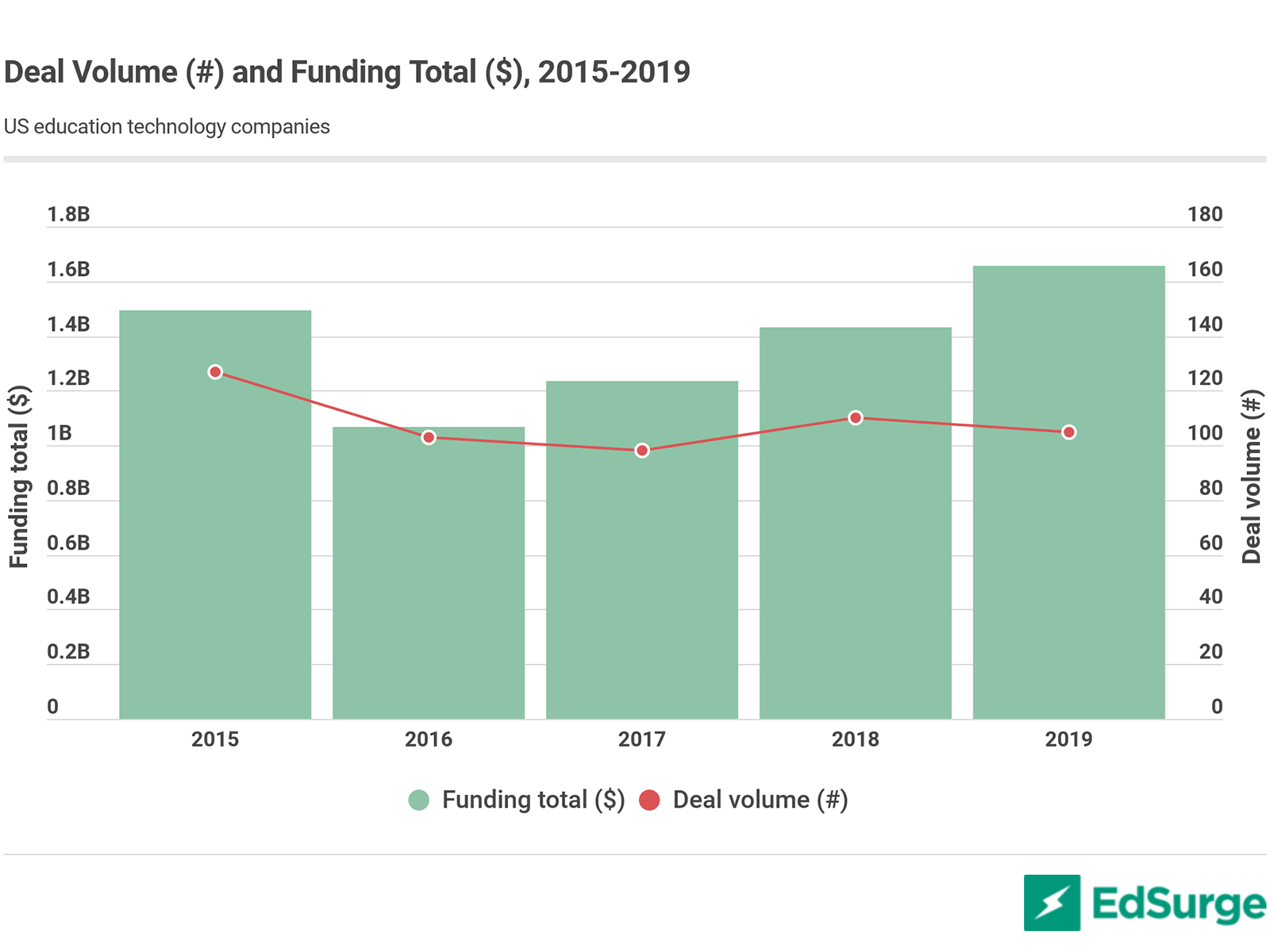

Finding and keeping good workers is more important than ever, and investors say these factors help explain a record year for venture capital in the U.S. education technology sector in 2019. According to an EdSurge database of publicly announced funding deals, investment in edtech companies reached at least $1.66 billion across 105 deals in 2019, a five-year high in value.

By dollars, 2019’s deal value saw a 16 percent increase from the previous year, even with five fewer less deals than 2018’s tally.

Blurred Lines

The influx of capital into the U.S. edtech industry in 2019 is largely mirrored across the broader venture capital landscape. A PwC-CB Insights report puts U.S. venture capital investments at $108 billion across 5,906 deals in 2019, the third-biggest year ever by value. Venture capitalists invested more money in 2018 and 2000.

For this year’s review, EdSurge looked at U.S.-based education companies that raised a round of at least $250,000. The analysis excluded individual tallies of funding from startup accelerators, which are often accounted for as companies raise funding rounds after they graduate from these programs. Companies that primarily offer financial and loan services that serve education as one of many markets were also not included.

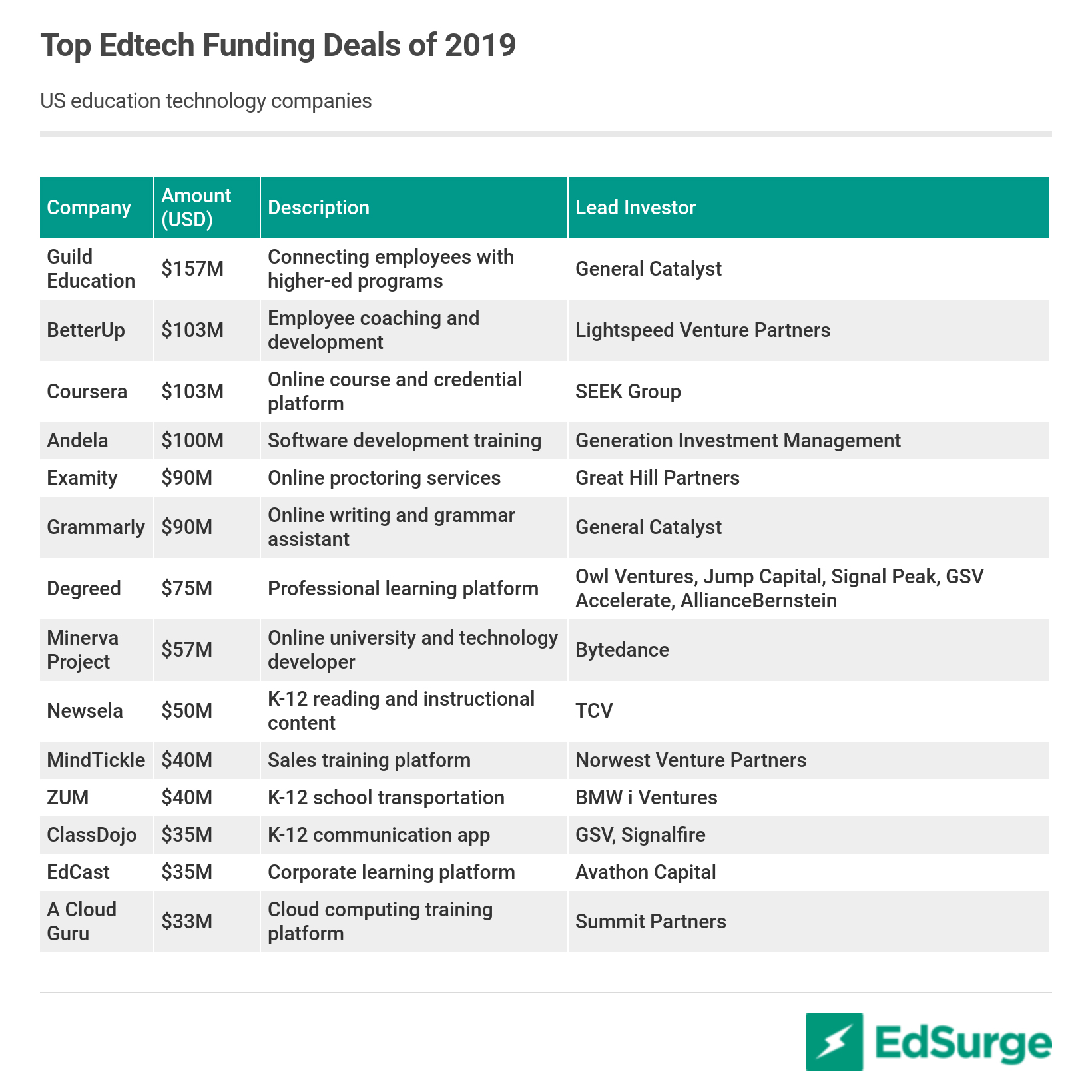

Eight of the top deals went to companies that offer educational services to employers and employees, typically focused on training them for purposes of retaining or internal promotion. Those elite eight—Guild Education, BetterUp, Coursera, Andela, Degreed, MindTickle, EdCast and A Cloud Guru—accounted for 39 percent of edtech investing in 2019.

Programs to train employees “are becoming table stakes for anyone who wants to run a company with great talent,” says Jenny Abramson, founding and managing partner of the Rethink Impact venture capital firm, which invests in edtech. “A retention of talent is going to matter.”

Last year saw four mega-rounds (exceeding $100 million), compared to two in 2018, three in 2017 and one the year prior. These four went to Andela, BetterUp, Coursera and Guild Education—companies that provide workforce training and development services.

“The lines between higher education and workforce are blurring,” says Jason Horne, managing director at GSV Advisors, which advises on financing and acquisition transactions for edtech companies. The blending of those markets “present big investment opportunities” that attract investors, for whom market size factors greatly into investment decisions, he says.

That middle ground is where 2019 chart-topper Guild Education plays. The Denver-based startup works with major corporations to connect their employees with degree-granting online courses offered by higher-ed institutions. Another big raiser, Coursera, has increasingly tailored its online higher-ed offerings to businesses that want to add to their employees’ skills.

Not as well represented in the top charts are companies serving the K-12 market. Other than school communication app ClassDojo, student transportation and Newsela, a provider of supplemental curriculum and leveled reading materials, most fundraises have been more modest. Yet at the same time, the K-12 market did see a number of notable exits late last year, including PowerSchool’s acquisition of Schoology and Renaissance Learning’s purchase of Schoolzilla.

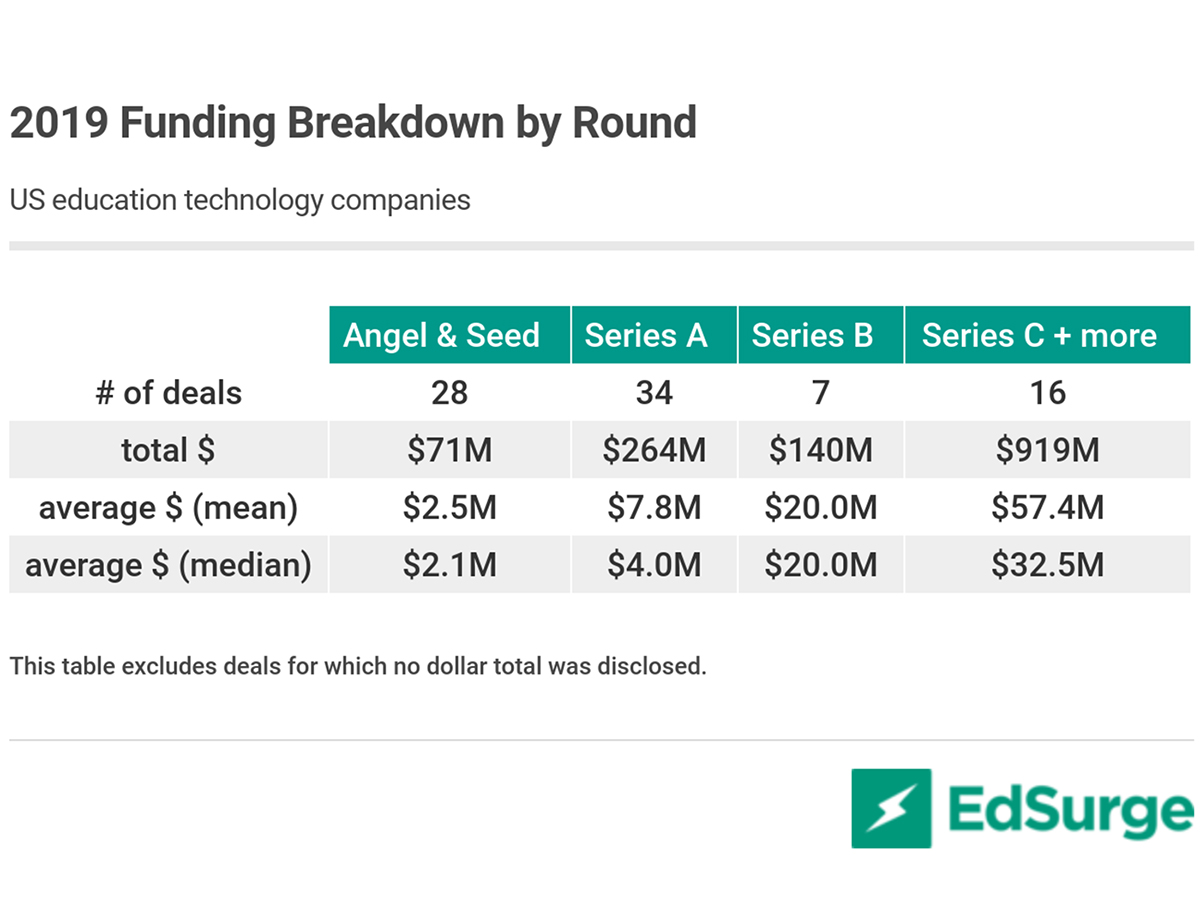

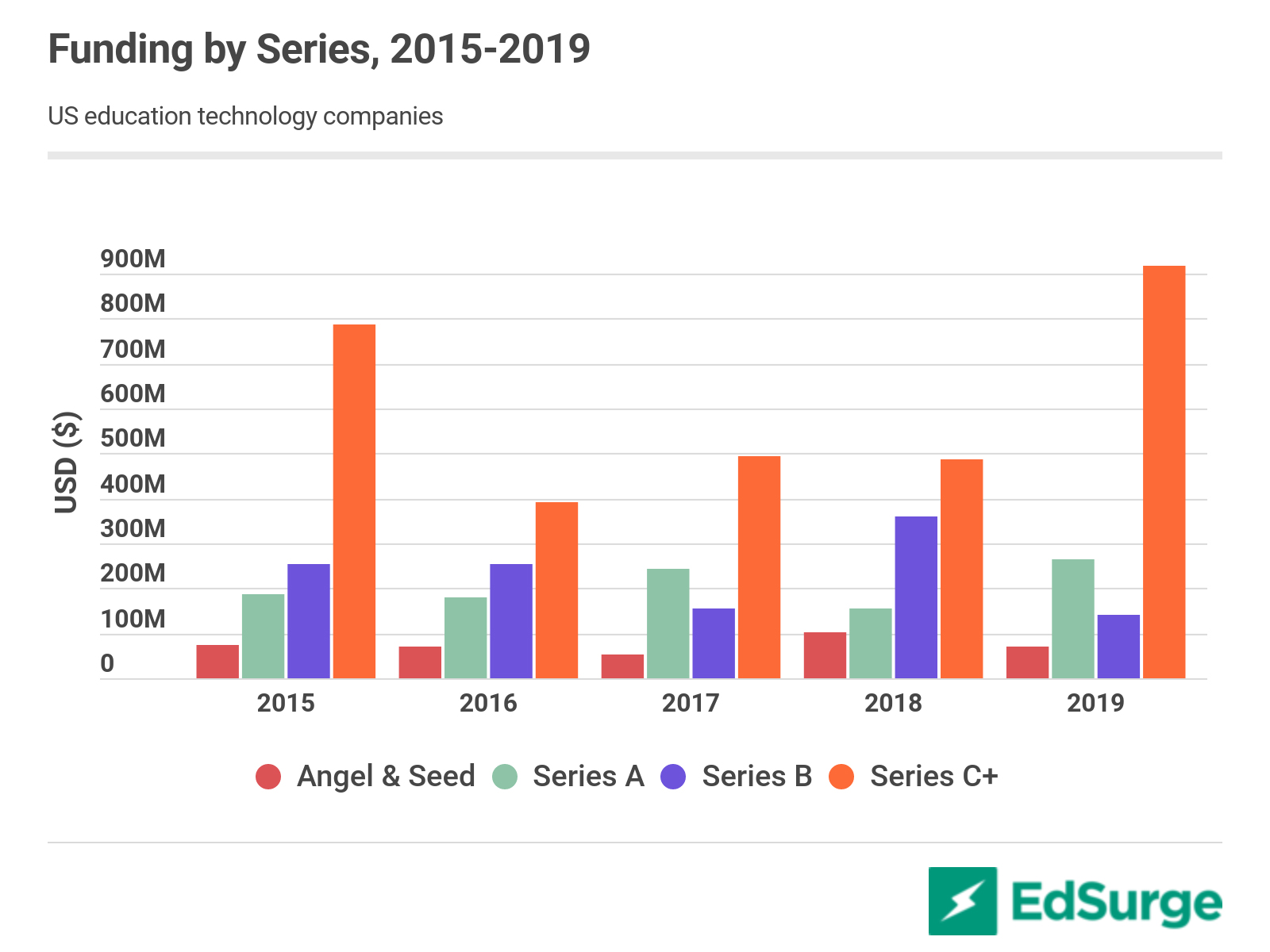

Overall, last year proved a windfall for companies raising Series C and subsequent rounds. Investors poured $919 million across 16 such disclosed deals last year, which surpassed the previous highs of $788 million raised across 13 deals in 2015.

The industry has also seen a marked increase in Series A funding, which had its highest tally over the past five years at $264 million. That’s an encouraging sign for seed-stage companies that have secured enough market traction.

On the other hand, last year witnessed a five-year low in the number of angel and seed rounds of at least $250,000—28, compared to 43 in 2018 and 45 in 2015.

A five-year low of seven Series B rounds occured in 2019 compared to the high of 17 in both 2016 and 2018.

Trends Not on the Charts

Among the companies to post top funding rounds, The Minerva Project is arguably the only company focused on higher education. But an opportunity to do business with colleges still exists. Investment bank BMO Capital Markets reported Thursday that the number of postsecondary students enrolled in exclusively distance education courses grew to 3.26 million in fall 2018 from 2.64 million students in fall 2012, with traditional public and private nonprofit universities accounting for over 80 percent of the fall 2018 total.

Though a gap still exists between higher education and careers, colleges have reacted to how quickly companies create new jobs, says Larry Lutz, executive vice president of corporate development and investments at Strada Education Network, which invests in edtech companies. Colleges “are increasingly partnering with employers to do that, and I think that’s going to continue,” he observes.

Filling that gap has been a factor in notable exits for coding bootcamps in 2019, including online program manager 2U’s purchase of Trilogy and college student services company Chegg’s purchase of Thinkful.

And opportunity exists at the opposite end of the age spectrum. Abramson predicts investment in childcare will continue to grow in importance as parents seek ways to balance raising a family with a day job. Last year saw one such major funding deal in Tinkergarten, a platform that helps parents find outdoor classes and activities for early learners. The company raised $21 million from a firm run by former bigwigs from DreamWorks and Dropbox.

Abramson’s not alone in watching early learning. According to the BMO report, childcare will be the fastest growing education sector over time. “We expect worksite childcare benefits will increase as a recruitment and retention tool, due to the tight labor market and improving demographics,” according to the report.

Wade Tyler Millward is a reporter at EdSurge covering edtech business. Reach him at wade [at] edsurge [dot] com.

Tony Wan (@tonywan) is Managing Editor at EdSurge, where he covers business and financing trends in the edtech industry. Reach him at tony [at] edsurge [dot] com.

Popular on Edsurge

Opinion