Education Technology Deals Reach $1.6 Billion in First Half of 2015

By Tony Wan and Tyler McNally

July 29, 2015

Shutterstock

Keeping tabs on education technology dealflow can be as confounding as counting calories: there are “good” and “bad” numbers, and some numbers mean more than others.

As part of our funding coverage, EdSurge keeps a close watch on dollars being invested in the edtech industry. Overall, venture capital for education technology companies has been on the rise for the first half of this decade. Even so, we’ve been surprised at the divergence around what should be simple facts, starting with the size of the edtech market.

Back in June, TechCrunch asserted that “investors seem to be taking a step back from the education industry in 2015.” A month later, CB Insights tallied a “new high for ed tech financing” in Q2 2015 at $765 million and suggested the industry is on pace for a record year. Not to be outdone, Ambient Insight counted more than $2.5 billion worth of edtech investments in the first half of this year alone. That figure surpasses Ambient’s reported edtech total for all of 2014.

By our tally, there were 161 edtech investments around the world during the first half of 2015, totaling $1.59 billion.

So, whose number will you believe?

*Through May 31, 2015

How can these market estimates differ by over a billion dollars?

Let’s start with how each define an “education technology” company. Just like this past spring’s viral debate over the color of the dress, there are many perspectives—and some debatable entries. For instance, Crunchbase currently includes a queuing management tool and photosharing app among its 1,400-plus edtech startups.

Ambient Insight offers a little more clarity into its selection process, which “only covers learning technology companies that develop instructional products directly involved in the learning process.” It does not count SoFi, which it defines as “financial technology,” or AltSchool because “it is a classroom-based brick-and-mortar operation.” But Ambient Insight does include Mapbox and Virgin Pulse—both of which raised over $50 million apiece. Their link to education is a bit tenous, though: Mapbox introduces educators to geomapping for free; Virgin Pulse offers behavior management software for adults.

For US companies, we counted 107 deals worth $1.1 billion in the first half of 2015.The point of these examples is not to haggle over which companies belong in the “edtech” category, but to highlight the nuances of the tallies. And expect the calculations to get more complicated as the boundaries between formal education and lifelong learning blur, and as enterprise tools find their way into schools.

All sources do agree on this: Big deals in China account for a significant chunk of ballooning dollar figures. As CB Insights noted, edtech is indeed booming for the Middle Kingdom, with the top ten deals in Chinese companies since 2014 totalling over $518 million. (Chinese investors are also taking a slice of American companies, too, as seen by the three China-based investors who led the $70 million Series B investment in the Minerva Project.)

What Is EdSurge Counting?

We define the scope of “edtech investments” to include all investments in technology companies whose primary purpose is to improve outcomes for all learners, regardless of age. We agree with Ambient Insight that Social Finance is more of a financial company than an education one. But we count AltSchool because it is using (and developing) technology to help students learn.

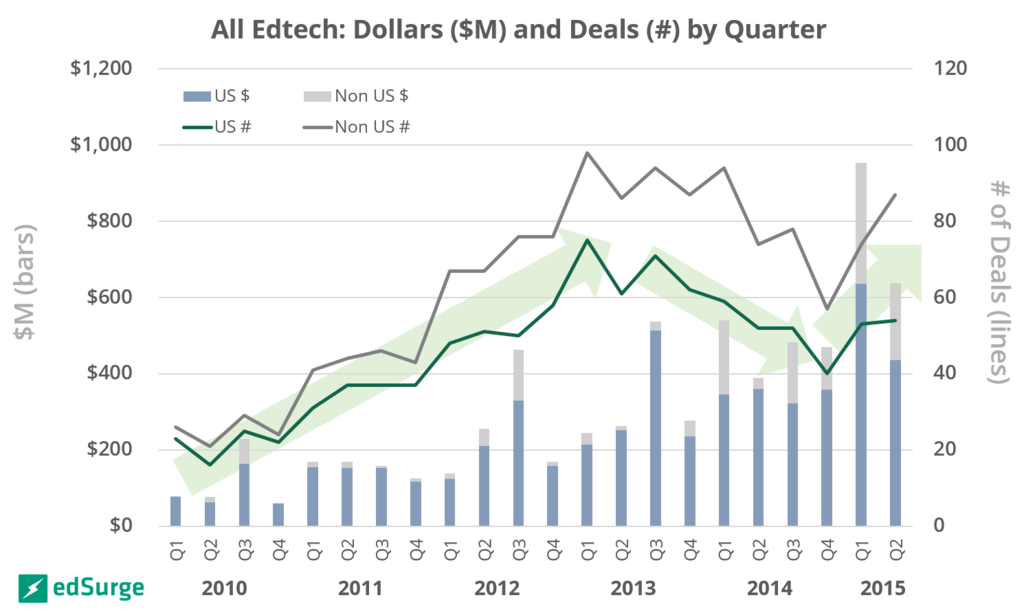

The following chart shows every deal we have in our database by quarter from Q1 2010 through Q2 2015.

Three distinct phases emerge: The number of deals increases nearly every quarter from Q1 2010 through Q3 2013, then slowly drifts down through Q4 2014 before resuming an upward trajectory during the first half of 2015. By contrast, the total dollars invested has been rising every quarter. In spite of a few outlier quarters, this upward trend averages approximately 20% quarter-over-quarter growth.

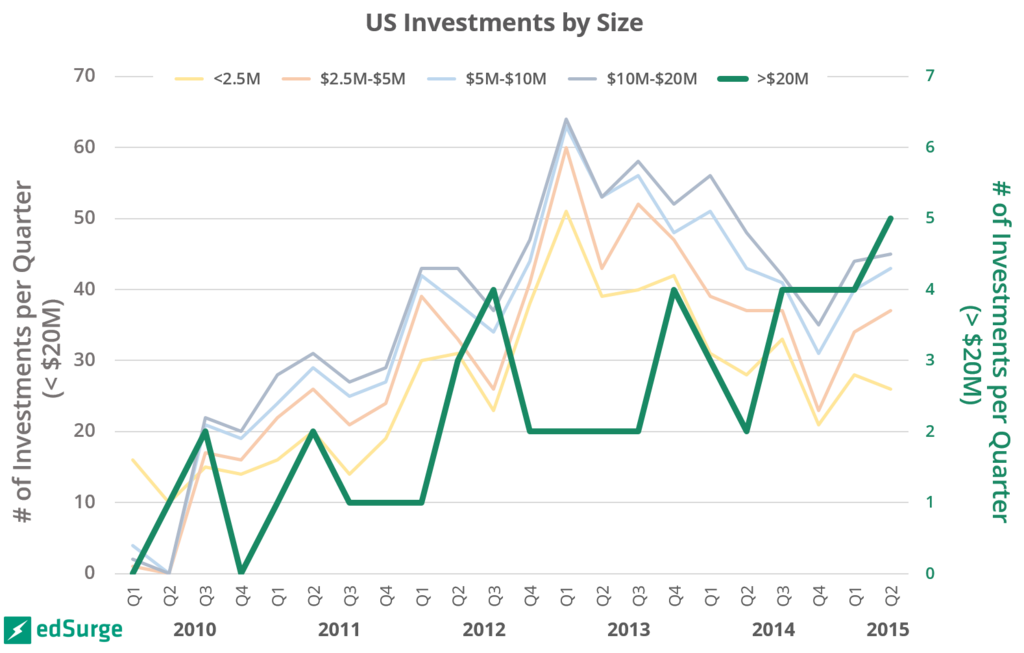

For US companies, we counted 107 deals worth $1.1 billion in the first half of 2015. Compared to 2013, the US edtech market has seen fewer deals, but bigger dollars—a sign of a maturing market. This year, for instance, we’ve seen several big B rounds, including AltSchool ($100 million) and littleBits ($44.2 million).

Seed rounds are growing bigger, too, and not just in edtech. K9 Ventures founder, Manu Kumar, who has noted this phenomenon, recently quipped that “ Seed is the New A.” Startups that recently raised sizable seed rounds include FreshGrade ($4.3 million), Panorama Education ($4 million) and MathCrunch ($3.5 million).

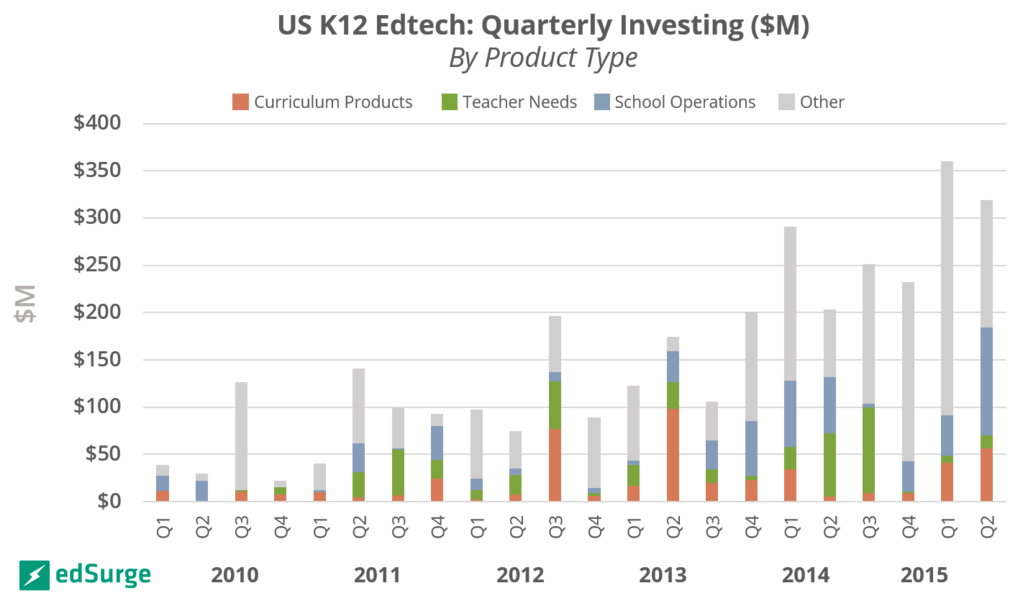

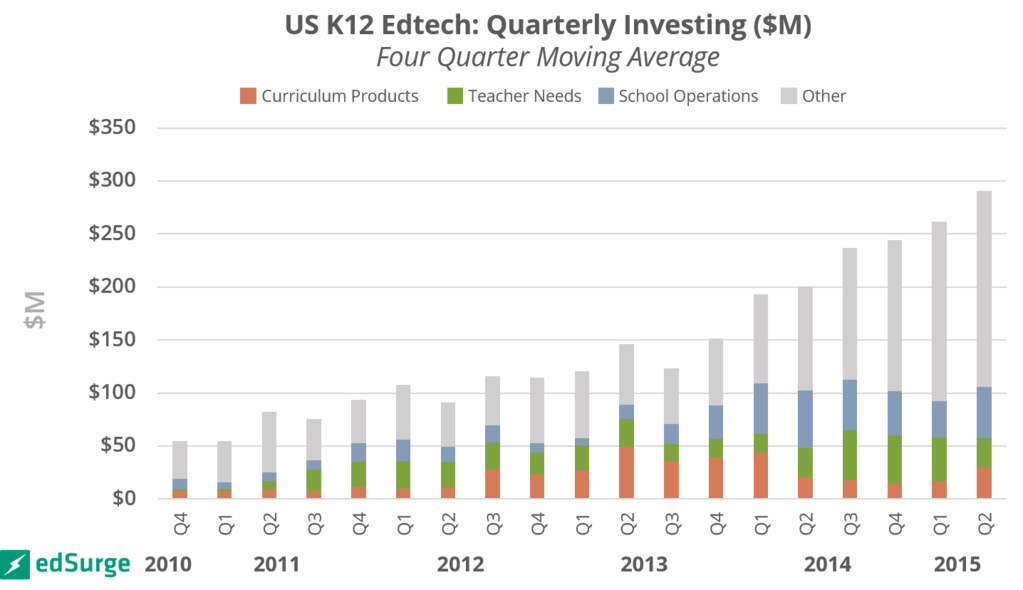

Looking Homeward: US K-12 Market

The overall US K-12 market has generally seen increasing dollars going into edtech per quarter, with outliers in the first quarters of 2014 and 2015.

At EdSurge, we categorize products into the following groups:

Curriculum Products: Content tools that teach specific subjects and skills

Teacher Needs: Products that help teachers with classroom-related activities such as grading, classroom management and lesson planning

School Operations: Products that are designed to help improve the management of schools, teachers, students and parents, primarily for use by principals and other school administrators

With an average of just 30 deals per quarter since 2010 and a very large difference between the smallest (e.g. $250,000) and largest deal ($25,000,000), long-term trends are hard to visualize. One way to get a better sense of the trajectory is to use a four-quarter moving average, which smooths out dramatic swings in one direction or the other to reveal the overall trend.

In the graph above, the data for each quarter represents the average funding for that quarter and the previous three. For example, the data for Q3 2011 is the average of Q4 2010, Q1 2011, Q2 2011 and Q3 2011. This chart illustrates that the total dollars invested in US K12 edtech have typically been rising with each quarter. Yes, a lot of that growth is driven by products we classify as “Other.” Even so, growth in non-curriculum products specifically designed for teachers, schools and districts is also increasing.

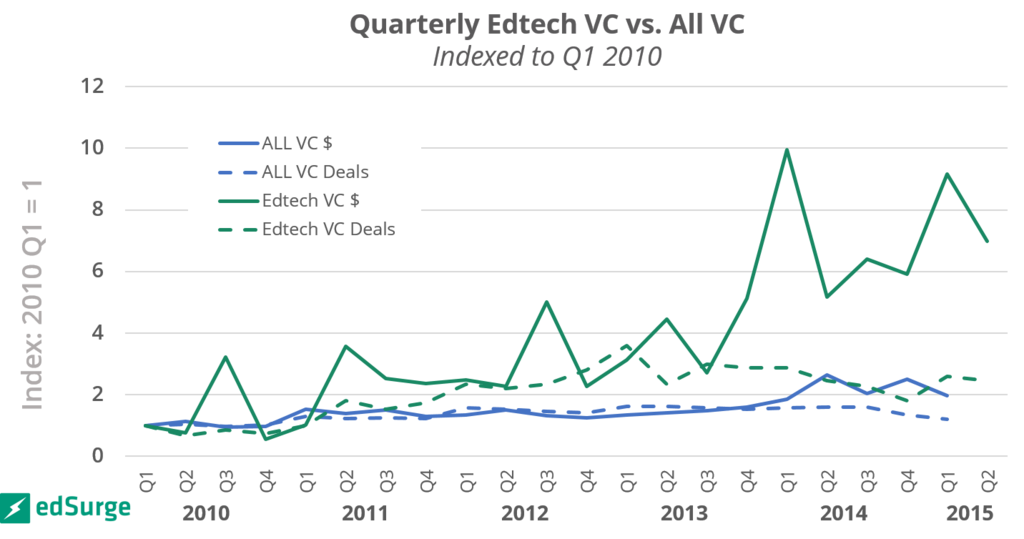

Finally, we wanted to see how funding activity for education technology has evolved over the last five years relative to funding in other (noneducation) sectors. The scale of investment (edtech versus nonedtech) is drastically different: In the first quarter of 2010, for instance, edtech investment totalled $22 million, a small drop in the water when compared to the $7 billion for all venture deals during that same time.

In the graph below, we indexed each of those Q1 2010 values ($22 million for edtech; $7 billion for all industries) to 1.0 and calculated how dollars changed in each quarter relative to Q1 2010. For example, if edtech investing doubled from $22 million to $44 million from one quarter to the next, the value would be “two.”

The growth in edtech investing over the past five years has been strong, particularly since 2013. Quarterly edtech investments are six to nine times higher than they were in 2010. By contrast, investments in across all sectors has grown much more slowly, doubling over the same period. That said, as a percentage of all investments, edtech is still relatively miniscule.

Reading the Crystal Ball

We expect to see more deals across all company stages, thanks in part to the addition of new funding opportunities from recently-launched programs like the Intel Education Accelerator and AT&T Aspire Accelerator. Entrepreneurs will also welcome several new edtech funds dedicated to participating in mid-to-late funding rounds, including:

Reach Capital, a for-profit spinoff from NewSchools Venture Fund that is looking to make follow-on investments. It’s led by a trio of women who ran NewSchools’ Seed Fund, which supported 42 early-stage companies.

Owl Ventures, whose founders trace their origins to Catamount Ventures, which has invested in six education startups.

Zuckerberg Education Ventures, which participated in AltSchool’s $100 million Series B round.

Disclosure: Reach Capital and Owl Ventures are investors in EdSurge.

An earlier version of this article listed Startup: Education as one of the firms that will invest in education companies. It has only invested in one company (Panorama Education).

Popular on Edsurge

Voices of Change