Are K-12 Curriculum Tools a Smart Investment? What Investors and Our Data Say

By Alex Sigillo

September 17, 2019

NosorogUA / Shutterstock

“Curriculum is becoming commoditized.”

So says Jason Palmer, a general partner at New Markets Venture Partners. And he’s not alone.

In conversations with edtech investors, some reported that the K-12 market has seen an influx of instructional content, particularly in the form of open educational resources (OERs). That can give them pause when it comes to investing in propriety K-12 curriculum products.

The increasing availability, accessibility and quality of OER materials offer districts the opportunity to move away from textbook publishers and develop their own curriculum. OERs are openly-licensed educational materials that can be downloaded, modified and shared with others to help support student learning.

The trend has won admirers in the upper echelon of the education system as well. Through the #GoOpen initiative, launched in 2015, the U.S. Department of Education has encouraged K-12 school districts to use OERs in the classroom, and free up funds typically spent on textbooks for other much-needed resources. With OERs, educators can become curriculum makers. Many tools give teachers the flexibility to customize lesson plans for their students by pulling in up-to-date content and activities, without waiting for the latest textbook versions to hit the market.

Curriculum is becoming commoditized

Jason Palmer

But many other investors are driven to invest in curriculum products because of their potential impact on student learning outcomes. They believe that schools and districts are better positioned to adopt digital curricula now than a few years ago. Investments in school technology infrastructure have made it possible to deploy online curriculum tools, as more schools have access to high-speed internet to support one-to-one devices, and more administrators opt to purchase digital instructional tools that offer personalized instruction.

These investors acknowledge that curriculum products with personalized content pathways can differentiate themselves from OERs. Further, the inclusion of pre-built assessments, school-level analytics or data visualizations can provide additional value on top of the digital instructional content.

Yet edtech investors remain uncertain whether to invest in K-12 curriculum products. Some are hesitant, as they believe more schools will use OER materials for instructional content. Others are more optimistic about the adoption of proprietary digital curriculum tools.

To better understand their perspectives, we dug into the numbers. In a year-long study, the EdSurge Research team, in collaboration with NewSchools Venture Fund, investigated where investment capital has been flowing in the U.S. K-12 edtech market over the past three years, the factors that are driving shifts in the market, and how investment trends might change in the near future.

We collected both qualitative and quantitative data to understand these market complexities, utilizing data from three different sources: Ka’ching (our internal investment database), interviews with investors, and a survey. (Learn more about this EdSurge Research project here.)

SourceDescription Ka’chingEdSurge tracks and reports on equity and debt investments in edtech companies across multiple education sectors and many countries. Each investment is collected in our Ka’ching database. (We do not track grants.)SurveyEdSurge developed a 33-question survey to understand investors’ perceptions of edtech funding trends in the U.S. K-12 market and for curriculum products in particular. There was a convenience sample of 81 survey respondents, 70 of which were valid. (Eleven respondents were disqualified because they did not invest in K-12 edtech companies.)InterviewsEdSurge conducted interviews to dive deep into the trends that emerged from the survey. We developed a standard interview protocol and used it to conduct one-hour phone interviews with 16 people who are involved in edtech investment decision-making from a diverse set of organizations.

What the Data Tells Us

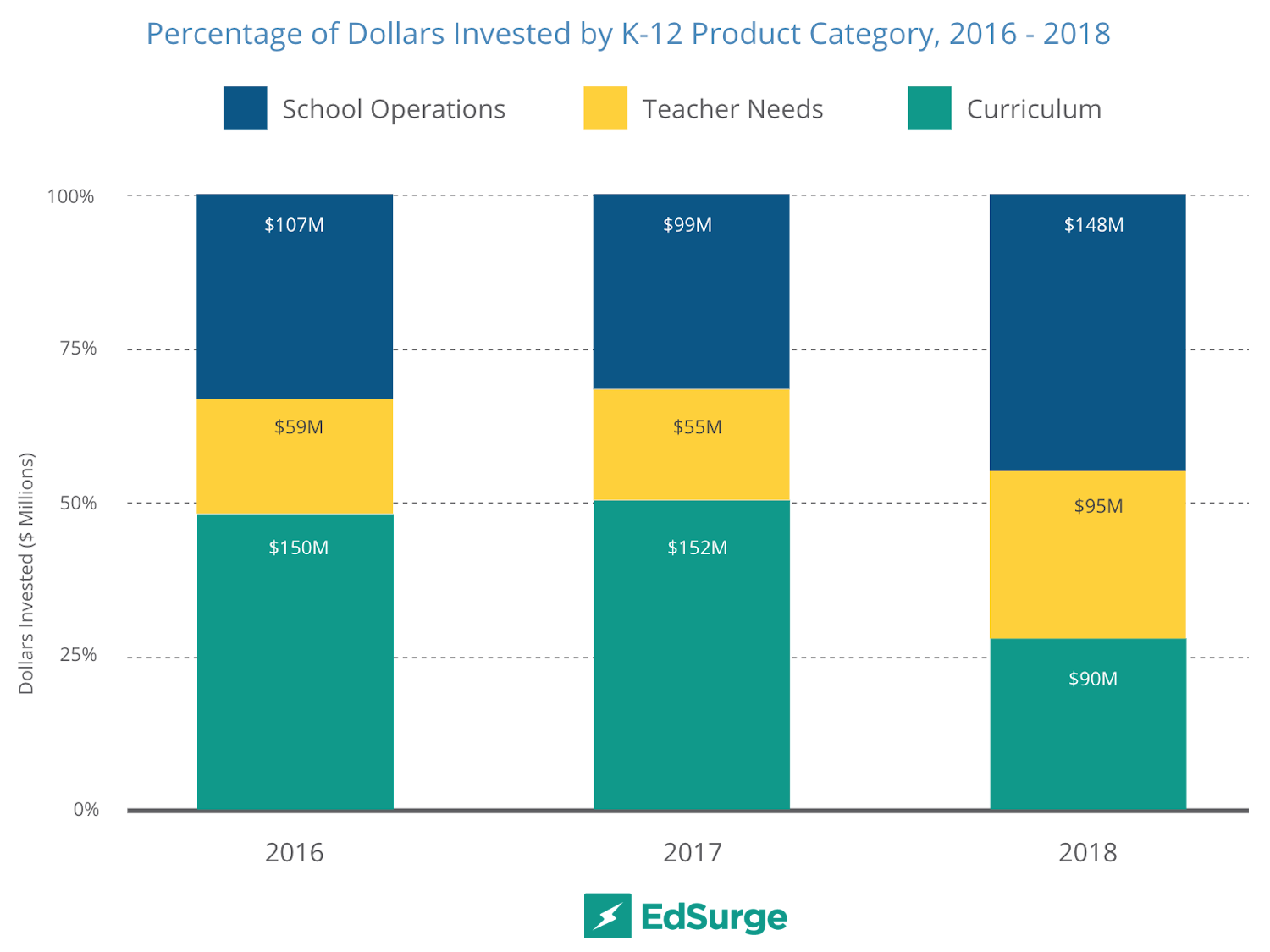

From 2016 to 2018, funding for products that support K-12 educators and learners has remained relatively flat—at around $318 million. But breaking down K-12 investments into more distinct categories, funding for curriculum products dropped from about 50 percent of the K-12 sector to just 25 percent, while funding for tools that support classroom teachers and products that streamline school operations has grown.

This dip in funding is particularly shocking for the camp of investors who consider that using digital curriculum products might have a positive impact on students’ learning.

Our analysis excludes mega deals, which refers to an investment that is $100 million or more. Because the deals are outliers that can skew analyses, we removed them in order to get a more accurate representation of trends in the edtech market. Within the past three years, three mega deals occurred in the curriculum space. In 2017, EverFi raised a $190 million Series D round and Grammarly nabbed a $110 million investment. Dreambox received $130 million in 2018.

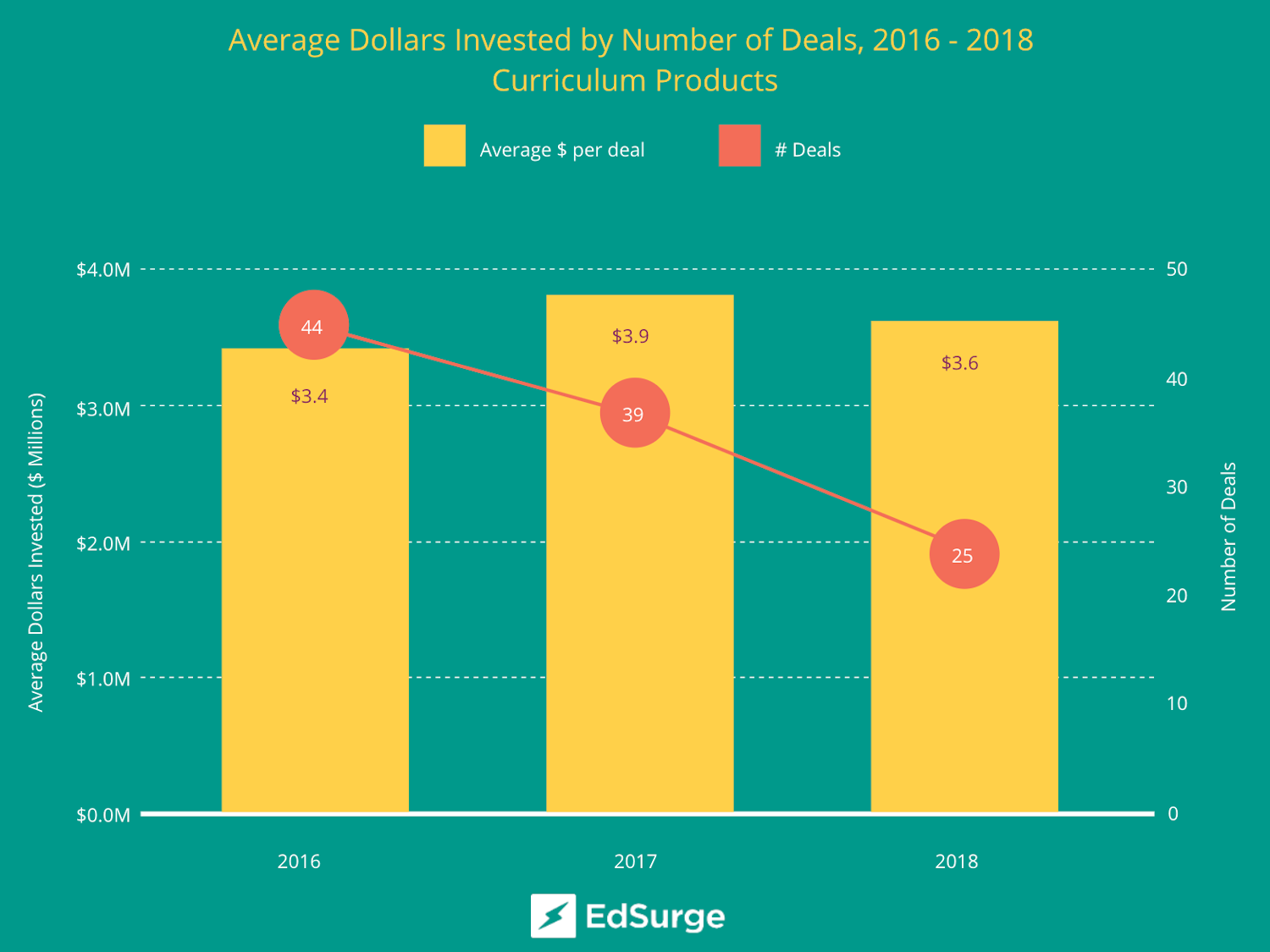

In terms of the volume of deals and their dollar totals, there have been fewer and fewer fundraises for K-12 curriculum—from 44 deals in 2016 to just 25 deals in 2018. That’s a 43 percent dip in the number of deals. By comparison, the average amount of dollars invested in each of these deals has remained relatively flat—at around $3.6 million—over the past three years. In other words, there have been fewer deals at similar average check sizes.

In 2016, the amount of dollars invested in K-12 curriculum products was $150 million. Last year, it was $90 million. What has caused the edtech market to decrease over the past three years? And more importantly, with fewer dollars invested, where is the money going? Is it targeted at the curricular areas that teachers feel are most impactful for learners?

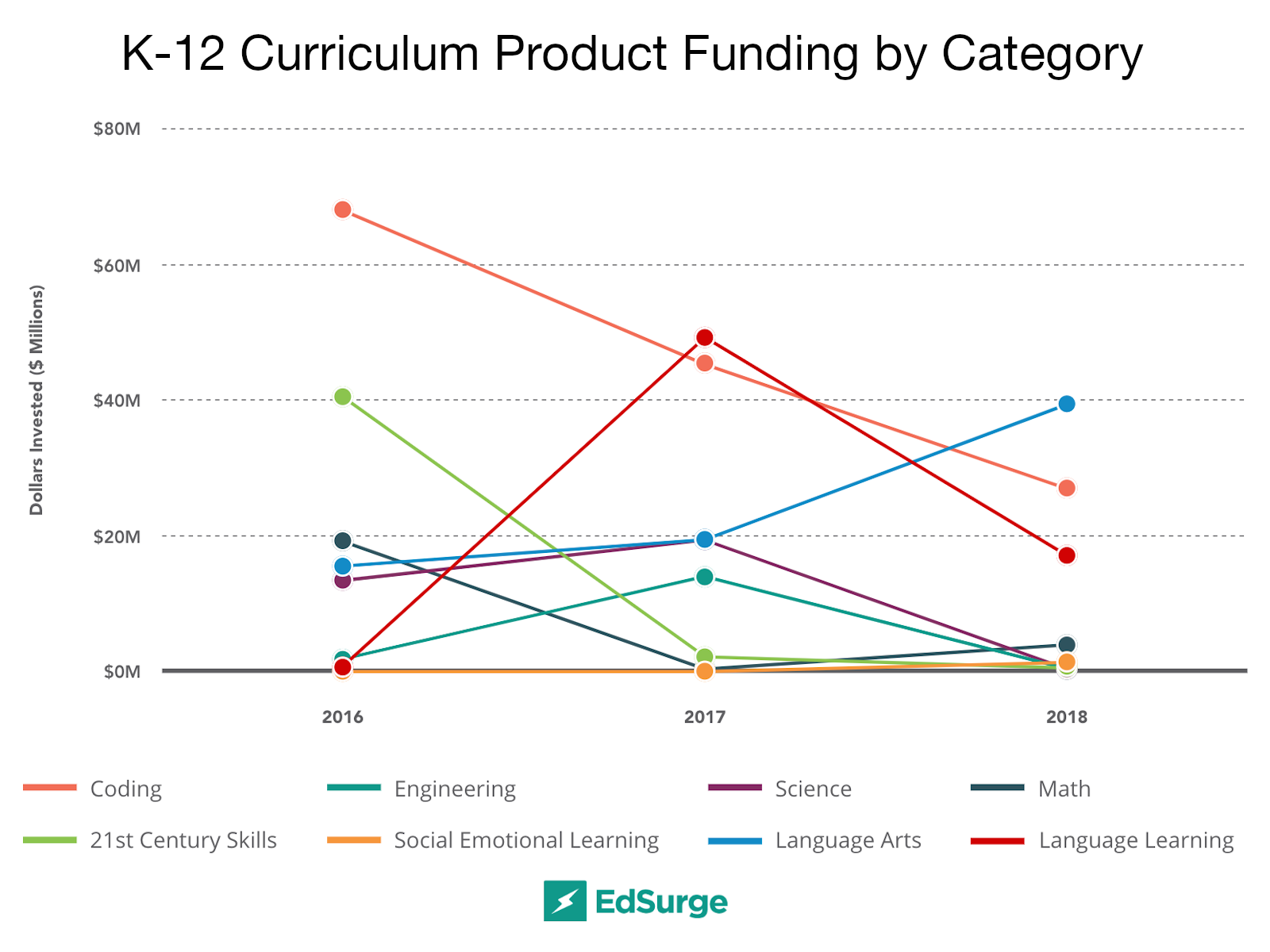

Products designed to teach coding, sequencing and programming languages have become the front runner when it comes to curriculum investments, even though funding in this area has been dropping since 2016. Investors see a greater potential return on investment with coding products, which is largely influenced by changes in both federal and state policies.

Funding for language arts products, by contrast, has seen a recent uptick. Products designed to teach reading, grammar and other English language knowledge and skills are likely to continue receiving investment, though we might expect to see the level of investment vary based on more specific content areas, such as writing and vocabulary. A focus on these specific content areas could be a “way in” for investors in an otherwise crowded English language arts market.

While philanthropic dollars are leading much of the support for social and emotional learning efforts, products that support the development of social-emotional competencies are just starting to see the first droplets of venture capital. Products that support areas such as identity development, emotional regulation and relationship building are emerging, along with the opportunity to invest in those products.

We’ve mapped venture capital dollars for each subject area to identify where money is flowing and where funding gaps exist. And how investors view curriculum—as a commodity or valued tool—influences whether they invest. See what other factors signal a smart investment by diving into our interactive website.

Disclosure: Jason Palmer is an investor in EdSurge.

Alex Sigillo (@dralexsigillo) is Research Project Manager at EdSurge.

Popular on Edsurge

Voices of Change